XiaoMi-AI文件搜索系统

World File Search Systemreasonable

独立从业者的保证报告Zalando SE遵守《数字服务法》

Deloitte GmbH Wirtschaftsprüfungsgesellschaft (hereafter ‘we', ‘Deloitte' or ‘independent practitioner') have been engaged by Zalando SE (hereafter ‘Zalando' or ‘audited provider') to perform a ‘reasonable assurance engagement,' as defined by International Standards on Assurance Engagements, to evaluate Zalando management's statement that the systems以及实施的过程,以遵守欧洲议会和理事会的2022/2065(EU)(EU)(“ ACT”或“ DSA”)(其“陈述”)(其“陈述”),并根据《系统和手动过程》第37条的规定(共同遵守规定的行为),并遵守该法案的规定,并提及(总体上),并提及(1)义务(1)(1)(1),并提及(1)(1)(1)(1)(1)(1)(1)(1)(1)(1)(1)(1),并提及(1)(1),并提及(1)(1),并提及(1)。 (“指定要求”)在08/25/2023至04/30/2024(“考试期间”)中。除非另有说明,否则每个适用的义务和承诺都定义在次级级别。

基于“双重碳”政策文本的定量分析

“双重碳”政策是实现“双重碳”目标的战略工具。“双重碳”政策的定量分析可以为制度设计和调整政策提供理论支持和决策参考,从而进一步改善“双重碳” 1 + N政策系统。By constructing a three-dimensional analysis framework of “ instrument-goal-object ” , adopting the content analysis method, and combining the coding results of the “ Dual Carbon ” policy text to conduct multidimensional cross-analysis, we found that the overall design of the “ Dual Carbon ” policy is reasonable, but at the same time, there are problems such as unbalanced distribution of policy instruments, incomplete coverage of policy goals, insuf fi cient政策对象的协同作用,政策维度之间的匹配程度较低。针对这些问题,提出了针对性的缓解措施。

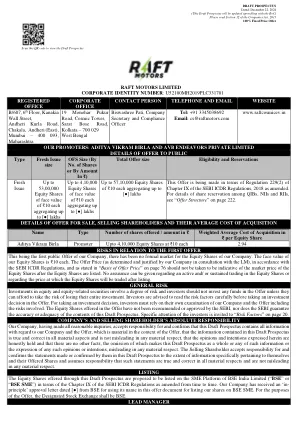

筏电机有限的公司身份编号

COMPANY'S AND SELLING SHAREHOLDER'S ABSOLUTE RESPONSIBILITY Our Company, having made all reasonable inquiries, accepts responsibility for and confirms that this Draft Prospectus contains all information with regard to our Company and the Offer, which is material in the context of the Offer, that the information contained in this Draft Prospectus is true and correct in all material aspects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts,省略使该招股说明书作为整体或任何此类信息或任何此类意见或意图的表达,在任何重大方面都有误导。销售股东承担责任并确认本招股招股法院草案中的陈述或确认的陈述,这些信息范围与自己及其所提供的股份有关,并承担责任,这些陈述在所有物质方面都是真实和正确的,并且在任何重大方面都不误导。

利用生成AI:商业秘密保护的最佳实践

商业秘密通常被理解为一个秘密的配方,例如饮食可乐或鸡肉酱的配方。但是,商业秘密包括大多数公司拥有的各种知识产权资产,包括客户列表,制造流程和营销策略。The Uniform Trade Secrets Act (the UTSA) defines “trade secret” as “information, including a formula, pattern, compilation, program, device, method, technique, or process that derives independent economic value, actual or potential, from not being generally known to, and not being readily ascertainable by proper means by, other persons who can obtain economic value from its disclosure or use, and is the subject of efforts that are reasonable under the circumstances to maintain its secrecy.”因此,商业秘密涵盖了各种规模的企业的许多宝贵资产,适当的保护至关重要。

Stanford Uniform Guidance Report FY2023_0.pdf

● Exercise professional judgment and maintain professional skepticism throughout the audit. ● Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, and design and perform audit procedures responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the consolidated financial statements. ● Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of Stanford's internal control. Accordingly, no such opinion is expressed. ● Evaluate the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluate the overall presentation of the consolidated financial statements. ● Conclude whether, in our judgment, there are conditions or events, considered in the aggregate, that raise substantial doubt about Stanford's ability to continue as a going concern for a reasonable period of time.

实施电子实施及其对供应的影响...

谈判是通过技术进行的合同协议;电子评估是收集有关供应商的广泛信息以进行进一步评估和交易的阶段。根据Chang等人(2012年),E采购可以在供应链管理中发挥战略作用,并为供应链绩效做出贡献。另一方面,通过E-采购增强供应链性能的方法在很大程度上不清楚。以下是理由:由于电子采购是一种电子(基于技术)的系统,因此电子采购的后果可以从供应链管理技术应用中得出(Presutti,2003)。先前的研究表明,关系交换策略,信息丰富的策略和联合学习策略可能是通过技术功能在供应链中采用的主要方法。As a result, it is reasonable to expect that data sharing, information enrichment, and joint-learning will be three essential strategies that businesses can utilise in e-procurement systems to improve supply chain performance.

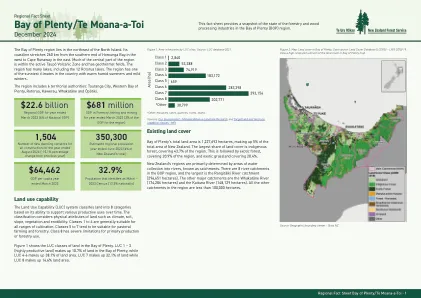

大量林业区域事实说明书

免责声明:此事实说明书和随附的所有信息(“事实说明))旨在仅与其他数据源和方法一起用作指南,并且只能用于开发其目的。此情况说明书中的信息基于从各种来源获得的数据摘要。While all reasonable measures have been taken to ensure the accuracy of the fact sheet, The Ministry for Primary Industries (MPI) (a) gives no warranty or representation in relation to the accuracy, completeness, reliability or fitness for purpose of the fact sheet, and (b) accepts no liability whatsoever in relation to any loss, damage or other costs relating to any person's use of the fact sheet, including but not limited to any compilations, derivative works or事实说明书的修改。皇冠版权所有©。此事实说明书受MPI管理的皇冠版权,使用此事实说明书根据CC BY-NC 4.0许可。

数据安全平台(SaaS)

•识别Varonis SaaS平台(“系统”)并描述系统的边界。•确定我们的主要服务承诺和系统要求。•确定将威胁到我们系统目标的主要服务承诺和服务要求的风险。•识别,设计,实施,操作和监视Varonis平台(系统)的有效控制,以减轻威胁实现主要服务承诺和系统要求的风险。•选择作为我们主张的基础的信托服务类别。We assert that the controls over the system were effective throughout the period August 1, 2023, to July 31, 2024, to provide reasonable assurance that the principal service commitments and system requirements were achieved, based on the criteria relevant to security, availability and confidentiality set forth in the AICPA's TSP Section 100 2017 Trust Services Principles and Criteria for Security, Availability, Processing Integrity, Confidentiality, and Privacy (2016).

弗吉尼亚州联邦...

4。(Expires December 31, 2023) The following costs incurred by the utility shall be deemed reasonable and prudent: (i) costs for transmission services provided to the utility by the regional transmission entity of which the utility is a member, as determined under applicable rates, terms and conditions approved by the Federal Energy Regulatory Commission [("FERC")], (ii) costs charged to the utility that are associated with demand response programs approved by the Federal Energy监管委员会由该公用事业公司的区域传输实体管理和管理,以及(iii)实用程序所产生的成本,用于建造,操作和维护安装的输电线路和变电站,以便为商业园区提供服务。在限期或终止上限费率后的任何时间请愿书,但在任何12个月的期间不超过一次,委员会应批准调整费率条款,该条款(包括不限制传输服务费用);新的和现有传输设施的费用,包括实用程序所产生的成本,以建造,操作和维护按顺序安装的传输线和变电站

第345号请愿书中的ROP/MP/2022&ORS。

(a)2018年6月22日的选择请求('rfs')由受访者Seci浮动,在其中,受访者Adani Hybrid Energy Jaisalmer One Limited(AHEJ1L)参加了上述RFS,并于2018年11月20日提交了其出价。在提交出价时,通知号2018年7月30日2018年7月30日的01/2018-CUSTOMS(SG)已经有效,根据该保障税,应在2年的进口太阳能电池中支付保障税,而价格在25%到15%之间。 在提交出价时,该项目的委托日期是颁发奖励信(“ LOA”)的18个月。 (b)通常,LOA的发行发生在电子逆转拍卖后的7-15天内。 但是,在本案中,电子逆转拍卖是在2018年12月15日进行的,并于2019年1月25日发布了LOA。 此外,根据RFS的第3.14.3条,PPA应在发行LOA之日起2个月内签署,并且PPA的生效日期应在LOA之后2个月。 但是,PPA仅在2019年11月28日延迟后才进入SECI和AHEJ1L之间,并且根据PPA为7.5.2021,预定的商业运营日期('SCOD')。 However, at the time of placing its bid, AHEJ1L had no reason to assume that there would be delays in the issuance of the LOA or signing of the PPAs, and as per the timelines envisaged in the RfS, the project completion date (COD) would have been 20.8.2020 giving merely 22 days' window between the Safeguard Duty cut-off date (29.7.2020) and COD. (c)即使LOA的实际发行日期,即 2019年10月25日。2018年7月30日2018年7月30日的01/2018-CUSTOMS(SG)已经有效,根据该保障税,应在2年的进口太阳能电池中支付保障税,而价格在25%到15%之间。在提交出价时,该项目的委托日期是颁发奖励信(“ LOA”)的18个月。(b)通常,LOA的发行发生在电子逆转拍卖后的7-15天内。但是,在本案中,电子逆转拍卖是在2018年12月15日进行的,并于2019年1月25日发布了LOA。此外,根据RFS的第3.14.3条,PPA应在发行LOA之日起2个月内签署,并且PPA的生效日期应在LOA之后2个月。但是,PPA仅在2019年11月28日延迟后才进入SECI和AHEJ1L之间,并且根据PPA为7.5.2021,预定的商业运营日期('SCOD')。However, at the time of placing its bid, AHEJ1L had no reason to assume that there would be delays in the issuance of the LOA or signing of the PPAs, and as per the timelines envisaged in the RfS, the project completion date (COD) would have been 20.8.2020 giving merely 22 days' window between the Safeguard Duty cut-off date (29.7.2020) and COD.(c)即使LOA的实际发行日期,即2019年10月25日。2019年1月2日,该项目的COD将以25.9.2020的速度运行,从而在保障责任截止日期和COD之间仅提供58天的窗口。 这清楚地表明,AHEJ1L在提交出价时,AHEJ1L已将保障义务施加了日期为2018年7月30日的通知。 (d)此外,根据RF的第3.16条,将在发行LOA之日起9个月内实现财务关闭。 因此,AHEJ1L在2019年10月25日实现财务关闭后,将下达购买太阳能电池的订单,当时保障税的现行税率为2018年7月30日的通知为20%。 因此,可以安全地得出结论,在财务出价时,AHEJ1L在竞标中考虑了以20%的税率的保障税。 (e) No prudent or reasonable generator will envisage that the date of issuance of the LOA and subsequent events pursuant thereto, such as execution of the PPA, may happen beyond the reasonable timeline, and therefore, there is no substance in even drawing a presumption that the generator would not have factored in prevailing duties essential for considering financial viability of the project.2019年1月2日,该项目的COD将以25.9.2020的速度运行,从而在保障责任截止日期和COD之间仅提供58天的窗口。这清楚地表明,AHEJ1L在提交出价时,AHEJ1L已将保障义务施加了日期为2018年7月30日的通知。(d)此外,根据RF的第3.16条,将在发行LOA之日起9个月内实现财务关闭。因此,AHEJ1L在2019年10月25日实现财务关闭后,将下达购买太阳能电池的订单,当时保障税的现行税率为2018年7月30日的通知为20%。因此,可以安全地得出结论,在财务出价时,AHEJ1L在竞标中考虑了以20%的税率的保障税。(e) No prudent or reasonable generator will envisage that the date of issuance of the LOA and subsequent events pursuant thereto, such as execution of the PPA, may happen beyond the reasonable timeline, and therefore, there is no substance in even drawing a presumption that the generator would not have factored in prevailing duties essential for considering financial viability of the project.