XiaoMi-AI文件搜索系统

World File Search SystemFICU

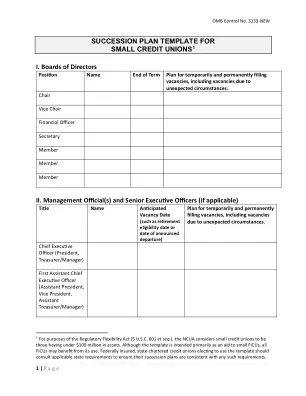

小型信用合作社继任计划模板1

1 就《监管灵活性法案》(5 USC 601 等)而言,NCUA 将小型信用合作社视为资产低于 1 亿美元的信用合作社。尽管该模板主要是为了帮助小型 FICU,但所有 FICU 都可以从中受益。选择使用该模板的联邦保险、州特许信用合作社应查阅适用的州要求,以确保其继任计划符合任何此类要求。

继任 - 规则-20241217.pdf

3 CUtoday.info, CUNA ACUC Coverage: What's Happening in Executive Compensation (June 19, 2019), https://www.cutoday.info/Fresh-Today/CUNA-ACUC-Coverage-What-s-Happening-in-Executive-Compensation.4 NCUA,信用合作社的信22-CU-05,骆驼评级系统(2022年3月),https://ncua.gov/Regulation-sustision-sustision-sustision-sustision-lectision-lectision-letsion-credit-credit-credit-unions-other-guidance/camels guidance/camels-rating-rating-System。骆驼是NCUA使用的评级系统的首字母缩写,以评估FICU的绩效和风险概况,这些绩效和风险概况来自FICU运营的六个关键要素:资本充足性,资产质量,管理,收入,流动性和对市场风险的敏感性。5 NCUA,信用合作社的信23-CU-01,NCUA的2023年监督优先级(2023年1月),https://ncua.gov/regulation-supervision/regulation-supervision/letters-credit-credit-unions-unions-other-gosother-the--other-guidance/ncuas-guas-guas-2023-supervisorvisory-priority。