机构名称:

¥ 1.0

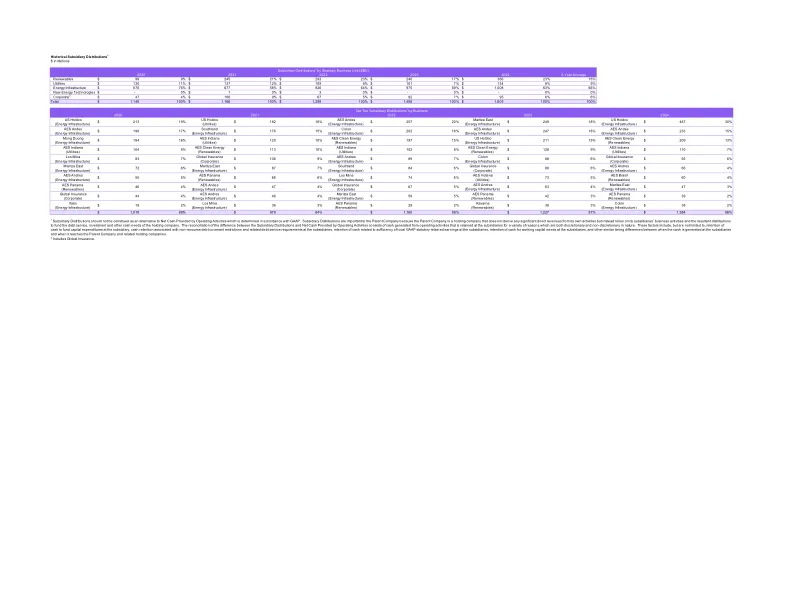

1个子公司分布不应被解释为根据GAAP确定的经营活动提供的净现金替代品。子公司分配对母公司很重要,因为母公司是一家控股公司,并未从其自身的活动中获得任何大量直接收入,而是依靠其子公司的业务活动以及由此产生的分配来资助债务服务,投资和控股公司的其他现金需求。通过运营活动提供的子公司分配与净现金之间的差额的核对由经营活动产生的现金组成,这些现金是由于各种自然界的酌情和非秘密性的原因而保留在子公司的。These factors include, but are not limited to, retention of cash to fund capital expenditures at the subsidiary, cash retention associated with non-recourse debt covenant restrictions and related debt service requirements at the subsidiaries, retention of cash related to sufficiency of local GAAP statutory retained earnings at the subsidiaries, retention of cash for working capital needs at the subsidiaries, and other similar timing differences between when the cash is generated at the子公司及其到达母公司及相关控股公司时。

历史子公司分布

主要关键词

相关文件推荐