XiaoMi-AI文件搜索系统

World File Search Systemauditors

截至 2024 年 9 月 30 日美国人事管理局合并财务报表的独立审计师报告

We conducted our audit in accordance with auditing standards generally accepted in the United States of America (GAAS), the standards applicable to financial audits contained in Government Auditing Standards , issued by the Comptroller General of the United States, and Office of Management and Budget (OMB) Bulletin No. 24-02, Audit Requirements for Federal Financial Statements . Our responsibilities under those standards and OMB Bulletin No. 24-02 are further described in the Auditors' Responsibilities for the Audit of the Financial Statements section of our report. We are required to be independent of the OPM and to meet our other ethical responsibilities, in accordance with the relevant ethical requirements relating to our audits. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

国家感染控制审计师的审计指南,用于医疗机构的审计策略,标准化方法作为更改的工具

Element # E-1 Medical Departmental Stores-------------------------------------------------------- 350 Element # E–2 Dietary Services Department*------------------------------------------------------- 354 Element # E–3 Laundry Department------------------------------------------------------------------ 369 Element # E–4 Mortuary Department----------------------------------------------------------------- 376 Element # E–5 Construction & Renovation Measures in Healthcare Facilities------------------ 383 Element # E–6 Housekeeping & Hospital Environment--------------------------------------------- 391 Element # E–7 Disinfectants & Antiseptics Supplies------------------------------------------------ 405 Element # E–8 Infectious Medical Waste------------------------------------------------------------- 407

宣布对非联邦审计员执行的已发生成本审计是否符合政府审计标准进行评估(项目编号 D2023-DEV0SO-0010.000)

2022 年 11 月 9 日 致国防合同审计局局长、国防后勤局局长的备忘录 主题:重新宣布对非联邦审计员执行的已发生成本审计是否符合政府审计标准进行评估(项目编号D2023-DEV0SO-0010.000) 我们重新宣布 2022 年 10 月 3 日宣布的主题评估(附件),以通知您非联邦审计员完成的审计样本期的变化。我们宣布的样本期是 2019 年 9 月 1 日至 2020 年 9 月 30 日,这是一个印刷错误。我们计划使用的样本期涵盖 2019 年 9 月 1 日至 2022 年 9 月 30 日。但是,评估范围(包括样本期)可能会发生变化,以确保我们实现评估目标。

国土安全部 2024 财年和 2023 财年合并财务报表和财务报告内部控制的独立审计报告

主题:独立审计师关于国土安全部 2024 财年和 2023 财年合并财务报表和财务报告内部控制的报告 所附报告介绍了对国土安全部 2024 财年和 2023 财年合并财务报表以及截至 2024 年 9 月 30 日的财务报告内部控制的综合审计结果。此项审计是 1990 年《首席财务官法案》所要求的,该法案经《国土安全部财务责任法案》(2004 年 10 月 16 日)修订。我们与独立公共会计师事务所毕马威会计师事务所 (KPMG) 签订了合同,由其进行审计。合同要求审计按照美国普遍接受的政府审计准则、管理和预算办公室审计指南以及 GAO/CIGIE 财务审计手册进行。本部门对所有财务报表均获得了无保留意见。然而,KPMG 对 DHS 的财务报告内部控制发表了负面意见,因为内部控制在三个方面存在重大缺陷。KPMG 还发现一个领域存在重大缺陷,并发现两起不遵守法律法规的情况。以下是 DHS 未遵守的重大缺陷、重大缺陷和法律法规的列表。

年度报告2020-2021年度报告2023-2024

“RESOLVED THAT pursuant to the provisions of Sections 139, 141, 142 and other applicable provisions, if any, of the Companies Act, 2013 read with the Companies (Audit and Auditors) Rules, 2014, and the Guidelines for Appointment of Statutory Central Auditors (SCAs)/Statutory Auditors (SAs) of Commercial Banks (excluding RRBs), UCBs and NBFCs (including HFCS)由印度储备银行(“ RBI”)发行。RBI/2021-22/25-参考。编号dos.co.arg/sec.01/01/08.91.001/2021-22 2021年4月27日,包括任何修正,修改或变化,M/s Bilimoria Mehta&Co。该公司在2027年举行的第109届年度股东大会的结论,但要按照其连续性履行适用的资格规范,并在此类薪酬上,这是公司董事会与联合法定审计师之间的共同商定的。

新闻稿2025年1月27日,AFRC研究提倡改善可持续性保证实践的倡导者,并敦促审计师纳入气候风险

新闻稿2025年1月27日,AFRC研究提倡改进的可持续性保证实践,并敦促审计师将气候风险纳入财务审计中,这会计和财务报告委员会(AFRC)今天发布了一项有关香港可持续性报告和保证的市场准备就绪的研究。在2024年12月,政府为大型上市实体和金融机构发布了路线图,以在2028年之前使用ISSB标准准备可持续性报告。作为绿色和可持续金融跨机构转向集团的成员,AFRC将为公众咨询的可持续性保证制定本地监管框架。这将增强对组织可持续性实践和报告的信誉和信心。了解市场对于制定强大的法规至关重要,该研究重点介绍了上市实体的可持续性报告和保证的准备,以及公共利益实体(PIE)审计师的准备就绪,以提供可持续性保证和实践,以应对财务审计中与气候相关的风险。这还允许AFRC确定能力建设的区域,以支持路线图实施。这项研究分为两个部分:首先,在Hang Seng Index(HSI)中对可持续性保证的分析,1和第二,对上市实体和派对审计师的实践和计划进行了两项调查。对具有派派参与的派审计师2和30.6%(797个响应)的调查率为89.3%(75个答复)。关键观察1。上市实体正在采取措施朝着强烈的气候报告,超过三分之一(37%)的被调查实体报告中度至高暴露于身体气候风险,例如洪水,台风和持续的高温。同样,有40%的人报告了旨在减轻或适应气候变化的政策,技术和市场变化的中度至高暴露风险。

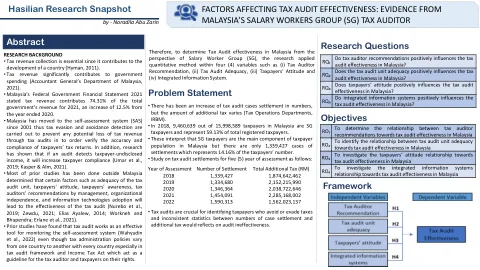

影响税收审计有效性的因素

determined that certain factors such as adequacy of the tax audit unit, taxpayers' attitude, taxpayers' awareness, tax auditors' recommendations by management, organizational independence, and information technologies adoption will lead to the effectiveness of the tax audit (Nurebo et al., 2019; Zewdu, 2021; Elias Ayalew, 2014; Workneh and Bhupendra; Erlane et al., 2021)。•先前的研究发现税收审计有效

2024-25年的培训计划日历(...

Training Programme on Financial Attest Audit Guidelines (including FAAM, audit using VLC and preparation of SFAR) (Auditors/ Accountants to Sr. AOs) 1 5 5 18 KC Topic – All India Training on Crypto Currencies 1 2 2 19 Works Audit and Contract Management 1 5 5 20 Audit of Autonomous Bodies 1 5 5 21 Workshop on Audit of Autonomous Bodies 1 2 2 22 Orientation Course 2 30 60 23 Administrative问题1 5 5

2020 年 - WendelGroup

" # "## #" " !@ Balance sheet – Statement of consolidated 6.1 financial position 338 Consolidated income statement 6.2 340 Statement of comprehensive income 6.3 341 Statement of changes in shareholders’ equity 6.4 342 Consolidated cash flow statement 6.5 343 General principles 6.6 344 Notes to the financial statements 6.7 345 Notes to the balance sheet 6.8 374 Notes to the income statement 6.9 394 Notes on changes in cash position 6.10 399 Other notes 6.11 402 Statutory auditors’ report on the consolidated 6.12 financial statements 409