XiaoMi-AI文件搜索系统

World File Search Systemborrower

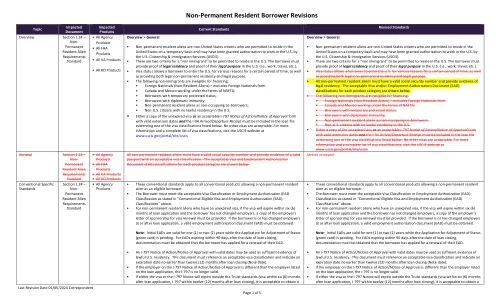

非永久居民借款人修订

•非永久性居民外国人是允许临时居住在美国的非公民公民,并可能已授予美国授权在美国工作公民与移民服务(USCIS)。•允许居住在美国的“非移民”有两个标准借款人必须提供合法居留权证明和在美国法律目的证明(即工作,旅行等)。•签证状况使借款人出于一定时间的各种原因进入美国,并提供合法的非永久居留权和法律目的。•以下非移民没有资格融资:•外国国民(非居民外国人) - 将外国国民排除在•加拿大和墨西哥根据北美自由贸易协定的条款工作; •具有临时保护状态的借款人; •具有外交免疫力的借款人; •非永久居民外国人作为非占领的共同借款人; •非U.S。在美国没有合法居留权的公民•未签证的副本或可接受的I-797诉讼通知/批准表的通知书,具有有效的延期日期,I-94到达/出发收据必须包括在下面列出的签证分类之一的贷款文件中。没有其他签证是可以接受的。有关更多信息和签证分类列表,请访问USCIS网站www.uscis.gov/portal/site/site/uscis

教育部借款人辩护解除

1 追踪:拜登-哈里斯政府下的学生贷款债务减免,CAP20(2024 年 9 月 4 日),https://www.americanprogress.org/article/tracker-student-loan-debt-relief-under-the-biden-harris-administration/。2 高等教育中的退伍军人学生,国家高等教育政策研究所(2023 年 11 月更新),https://pnpi.org/wp-content/uploads/2023/11/VeteransFactSheet-Nov-2023.pdf;学生借款人保护中心,绘制剥削地图:考察营利性大学作为有色人种社区金融掠夺者的情况 9(2021 年 7 月),https://protectborrowers.org/wp-content/uploads/2021/07/SBPC-Mapping-Exploitation-Report.pdf。 3 新闻稿,美国教育部,拜登-哈里斯政府批准向 317,000 名就读艺术学院的借款人提供 61 亿美元的团体学生贷款减免(2024 年 5 月 1 日),https://www.ed.gov/about/news/press-release/biden-harris-administration-approves-61-billion-group-student-loan。

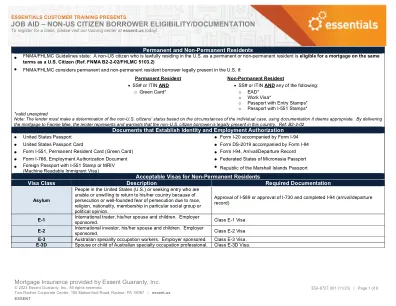

就业援助 – 非美国公民借款人资格/文件

• 已获批准并附有适当背书的 I-590 或已获批准的 I-730,以及 • 已完成的 I-94(入境/离境记录),以及 • 未过期的 EAD 或可接受的 I-9 文件(就业资格核查批准)。注意:仅适用于难民。I-94A 表格包含未过期的难民入境印章或计算机生成的 I-94 表格打印件,入境类别为“RE”,可向雇主出示,作为等待 EAD 期间工作许可的证明,有效期自雇用之日起 90 天。T-1 严重人口贩运的受害者。T-1 类签证。

HR 3564 – 2023 年中产阶级借款人保护法案

政府强烈反对 HR 3564。该法案将限制联邦住房金融局应对不断变化的住房市场条件的能力,并削弱该机构确保政府支持企业安全和稳健的能力。HR 3564 还将对联邦住房金融局的权力施加新的限制,使其难以为低收入和中等收入家庭和农村社区提供服务,也无法促进经济适用房的保护和预制住房。

支持印度国家绿色氢能计划

Pillar 1: Promoting Green Hydrogen • PA1: The Borrower has approved the NGHM • PA2: The Borrower has issued GH safety regulations, standards, codes , best practices, and procedures • PA3: The Borrower has notified extension of the waiver of the inter-state transmission charges towards RE for GH Pillar 2: Scaling Up Renewable Energy • PA4: The Borrower has issued a government order on RE Purchase Obligations and Energy Storage Obligations • PA5: The Borrower has issued and notified the Ancillary Services Regulations • PA6: The Borrower has issued a regulation to guide the bidding of 50 GW of RE capacity each year FY23-28 • PA7: The Borrower has adopted an offshore wind strategy; and has extended the waiver of the inter-state transmission charges for offshore wind • PA8: The Borrower has issued a policy to provide production-linked incentives to high-efficiency solar PV Pillar 3: Enhancing climate financing for low-carbon energy investments • PA9: The Borrower has amended the Energy Conservation Act that provide the legal framework for the launch of a national carbon market • PA10: The Borrower has issued amendments to the existing regulatory framework for Green Debt Securities issuance • PA11: The Borrower has issued a transparent Sovereign Green Bond Framework

销售指南

Section B2-1.1, Occupancy Types 158 ........................................................................................................................ B2-1.1-01, Occupancy Types (10/05/2022) 158 .....................................................................................................Section B2-1.2, LTV, CLTV, HCLTV, and Subordinate Financing 162 ............................................................................ B2-1.2-01, Loan-to-Value (LTV) Ratios (06/01/2022) 162 ....................................................................................... B2-1.2-02, Combined Loan-to-Value (CLTV) Ratios (12/04/2018) 164 .................................................................... B2-1.2-03, Home Equity Combined Loan-to-Value (HCLTV) Ratios (02/23/2016) 165 ............................................ B2-1.2-04, Subordinate Financing (05/03/2023) 167 ..................................................................................................................................................................Section B2-1.4, Loan Amortization Types 189 ............................................................................................................. B2-1.4-01, Fixed-Rate Loans (12/14/2022) 189 ...................................................................................................... B2-1.4-02, Adjustable-Rate Mortgages (ARMs) (12/14/2022)190 ............................................................................................................................................................................................................................................................................... ........................................................................................................Section B2-1.3, Loan Purpose 171 ............................................................................................................................... B2-1.3-01, Purchase Transactions (12/16/2020) 171 ............................................................................................. B2-1.3-02, Limited Cash-Out Refinance Transactions (12/11/2024) 174 ................................................................ B2-1.3-03, Cash-Out Refinance Transactions (02/01/2023) 180 ............................................................................ B2-1.3-04, Prohibited Refinancing Practices (08/04/2021) 185 .................................................................................................................................................................................................................................Citizen Borrower Eligibility Requirements (07/28/2015) 226 .................................................... B2-2-03, Multiple Financed Properties for the Same Borrower (06/01/2022) 226 .................................................. B2-2-04, Guarantors, Co-Signers, or Non-Occupant Borrowers on the Subject Transaction (09/02/2020)Section B2-1.5, Other Loan Attributes and Related Policies 206 ................................................................................. B2-1.5-01, Loan Limits (02/02/2022) 206 ............................................................................................................... B2-1.5-02, Loan Eligibility (06/05/2024) 207 ......................................................................................................................................................................................................................................................................... ...................................................................................................... B2-1.5-05, Principal Curtailments (11/06/2024) 222 .............................................................................................. Chapter B2-2, Borrower Eligibility 223 .............................................................................................................................. B2-2-01, General Borrower Eligibility Requirements (12/14/2022) 223 .................................................................. B2-2-02, Non–U.S.

信用及担保合同

这是您与贷款人之间具有约束力和可执行性的合同。在签订本合同之前,我们建议您寻求独立的法律建议。本信贷和担保合同由贷款人与您(借款人)于下表(附表 B)所示的日期签订。本信贷和担保合同包括但不限于:附表 A - 车辆说明、附表 B - 购买车辆的贷款预付款、附表 C - 担保契约、附表 D - 消费者信贷合同披露声明、附表 E - 机械故障保修、附表 F - 保险详情、附表 G - 近亲属详情以及不时需要的任何其他附件。背景 - 应借款人的要求,贷款人同意向借款人提供附表 B 所示的全部预付款,以使借款人购买附表 A 所示的车辆。借款人作为附表 C 中详述的个人财产担保的所有者,已同意将该财产(包括车辆)的担保权益授予贷款人。义务 - 借款人(若超过一个则为连带义务)承认其对贷款人负有附表 B 所列的全部预付款的债务,并承诺按照下列附表及其任何变更中规定的方式支付该金额以及本《信贷和担保合同》项下到期的任何其他金额,并承诺遵守本合同的条款和条件。

单户MBS披露指南 - 资本市场

L-023借款人信用评分在贷款发起过程中用于评估借款人的标准化信用评分。单个借款人的标准化信用评分或代表性的信用评分是i)如果从借款人的两个信用评分存储库中获得得分,则两个分数的较低,或II)如果从借款人的三个信用评分存储库中获得分数,则三分。对贷款的每个借款人进行了此评估。•将披露所有借款人的最低代表性信用评分•对于所有新交付的贷款,房利美都使用Fair Isaac Corporation开发的“经典” FICO评分,其范围为300-850。

改善和标准化抵押再融资

同一启发者再融资,如果借款人由于迅速上涨的保险付款而具有托管帐户赤字,则发起人可以选择允许相同的追赶计划,就像借款人没有再融资一样。如果与不同发起人的借款人再融资,他们通常必须提出全额资金来资助托管帐户,通常是两到三个月的税款和保险。旧服务人员通常会在30天后将托管帐户汇出到借款人。延迟是确保没有其他义务。但是,这种时机不匹配是当今技术不必要的,因为预先已知的金额。改革托管系统的主题不仅仅是再融资。我们打算在将来的出版物中解决它。