机构名称:

¥ 1.0

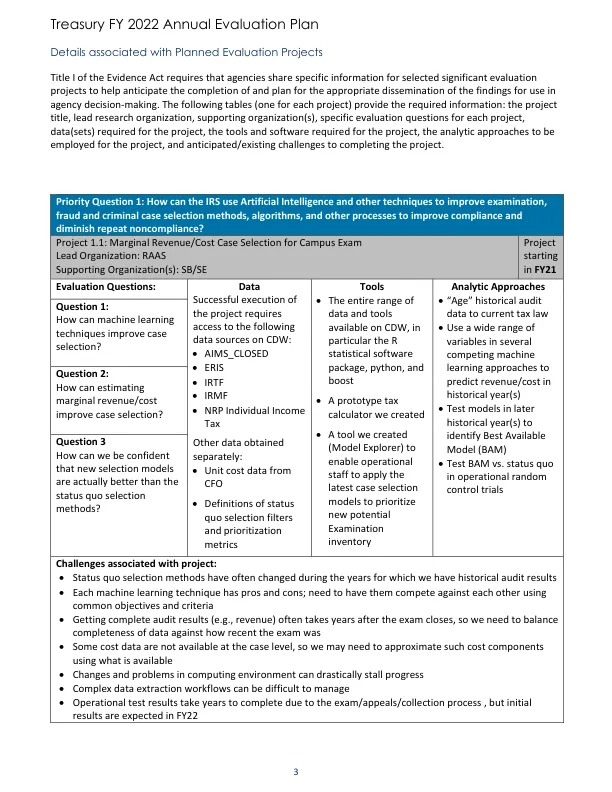

•现状选择方法经常在我们获得历史审计结果的几年中发生了变化•每种机器学习技术都有优点和缺点; need to have them compete against each other using common objectives and criteria • Getting complete audit results (e.g., revenue) often takes years after the exam closes, so we need to balance completeness of data against how recent the exam was • Some cost data are not available at the case level, so we may need to approximate such cost components using what is available • Changes and problems in computing environment can drastically stall progress • Complex data extraction workflows can be difficult to manage • Operational test results take years要完成考试/上诉/收集过程,但初始

财政财政部2022年度评估计划

主要关键词

相关文件推荐