机构名称:

¥ 5.0

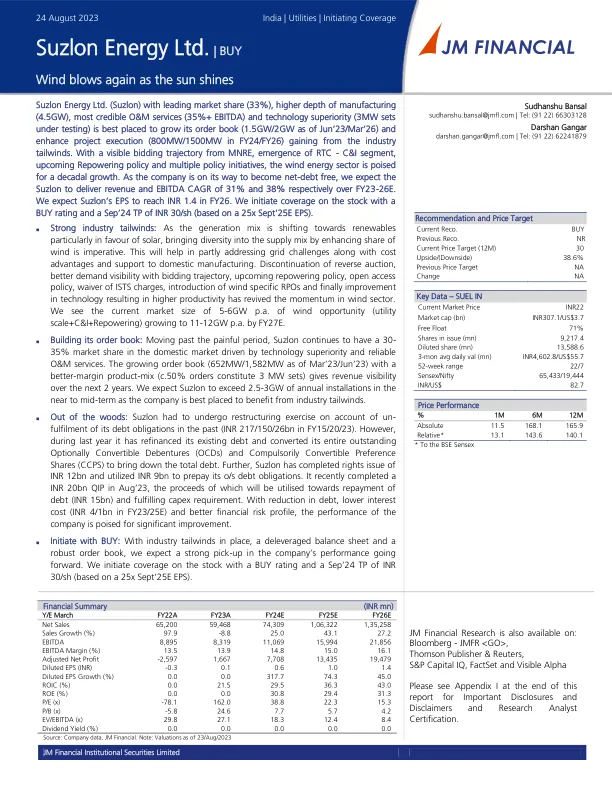

Suzlon Energy Ltd. (Suzlon) with leading market share (33%), higher depth of manufacturing (4.5GW), most credible O&M services (35%+ EBITDA) and technology superiority (3MW sets under testing) is best placed to grow its order book (1.5GW/2GW as of Jun'23/Mar'26) and enhance project execution (800MW/1500MW in FY24/FY26)从行业的方风中获得。随着MNRE的可见招标轨迹,RTC -C&I细分市场的出现,即将到来的重新制定政策和多个政策计划,风能领域有望实现十年的增长。由于该公司即将获得净销售净额,因此我们预计Suzlon将在23-26E中分别提供31%和38%的EBITDA CAGR。我们希望Suzlon的EPS在26财年达到1.4 INR。我们以买入评级和9月24日的30印度卢比(基于9月25日的EPS)对股票进行覆盖范围。

Suzlon Energy Ltd. -JMFL研究门户

主要关键词

相关文件推荐